Disclaimer: I am not a financial analyst, accountant, lawyer, economist, marketer, or similar. I am simply an individual who has followed Safex for some time now and have invested time into researching the crypto and e-commerce fields. I am not affiliated with the Safex team. My opinions are my own and I have referenced my claims to the best of my ability. Please enjoy. – znffal

Soon we will enter a new era of online selling; crypto commerce. As I have previously discussed, the world of e-commerce is in the middle of unprecedented growth [1, 2], and soon people will regularly be buying and selling online with crypto currencies. Safex aims to tap into this giant market and to become the leader in crypto commerce [3]. This article is aimed at the early investors in Safex.

If, in May 1997, you had invested $1000 into Amazon shares (@ $1.73 each) you would today be a millionaire. We do not yet know what your return on investment (ROI) will be if someone was to buy $1000 worth of Safex tokens today, but we know one thing; Safex has the potential to become a big player in the world of online selling.

As an investor into Safex, we are buying into a vision of fast, cheap, safe, secure, and private online shopping, and for some of us, a vision of a new kind of company. The Safex resident economist, Ivana Tudor stated it this way:

“Unlike the traditional company model where a single person gains the outcome of a business. Safex is like a public utility and the public holders of the Safex coin earn the outcome of the marketplace. All people involved are each sharing the yields of the development.

The Safex development model solves a major problem known as the Principal-Agent Problem and the Safex enterprise that is directly a member of the community has the same interest as each holder of the Safex coin and the marketplace’s success.” – https://medium.com/@ivanatudor/safex-dividend-calculator-why-what-and-how-b71f381fd33

In other words, any profits generated by the Safex marketplace and ecosystem are distributed proportionally to the investors (those who hold the Safex token), rather than to the company itself. For investors this is a massive opportunity to potentially earn a passive or replacement income from the payments from the Safex marketplace profits. Let’s look at the mechanics of these “incentive” payments.

Explanation of “incentives”

The Safex Blue Paper [4] describes the mechanism of these incentive payments. As quoted in the blue paper:

“…someone with Safex Tokens can “lock in” their tokens and begin receiving fees from the marketplace… the tokens can be unlocked from the blockchain”.

The cost to lock in any number of owned tokens to earn incentives is one Safex token, and while this one token then becomes unspendable, it does continue to earn incentives. It is also possible to unlock tokens for a further one Safex fee. Each lock or unlock transaction will cost one Safex token.

An important point to emphasise here is that your tokens only earn incentives if they are locked in. Any tokens that are unlocked (for example, if they are being traded on an exchange) do not receive incentives. Any “unclaimed” incentives are automatically distributed to those tokens which are locked in.

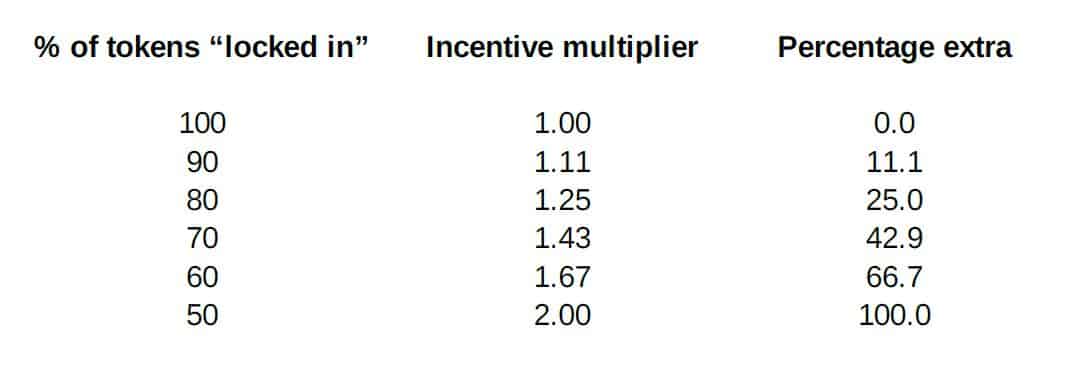

As an example, suppose that $21,474,836.47 in fees is generated on the marketplace. Then each Safex token (out of the total supply of 2,147,483,647) is eligible for an effective 1 cent incentive payment. However, if only 70% of Safex tokens are locked in, then the 30% that are not locked in lose their incentive payment, and the 70% that are locked in would receive an incentive payment of approximately 1.43 cents per token.

The calculation for incentive payments is “Total marketplace fees / Total locked in Safex tokens”. Since the number of locked in tokens is in the denominator of the fraction, the effect of unlocked tokens is not one-to-one. What I mean is, if 20% of tokens are unlocked and hence, 20% of tokens are not receiving incentives, the locked in tokens actually earn with a multiplier of 100/80 = 1.25 (i.e. 25% extra incentive payment than if all tokens were locked in).

As mentioned in the Blue paper, these incentive payments originate from the fees charged on the marketplace:

“Incentives are established from charging a 5% marketplace fee, this is a provision on all sales offers of goods and services on the platform. At the conclusion of payment the provision is allocated proportionally to all locked in Safex Tokens”.

It is my understanding that these incentive payments will be distributed daily in the form of the Safex Cash token.

Incentives do not depend on Safex token market cap (mostly)

During a conversation with some members of the community (mostly with Skero on Discord / @RockellerMS on Twitter), I was reminded that the incentive payment is effectively independent of the value of the Safex token.

By this I mean that the total value of the incentives paid per day is not tied to the value of the Safex token (say, on CoinMarketCap), but on the value of sales made using the Safex Marketplace.

The value of the Safex Token is likely to rise as the incentive payment is larger, but the marketplace volume (and hence the total incentive payment) does not necessarily rise or fall depending on the rise and fall of Safex Token price.

This effectively provides more certainty for Safex investors, particularly in a “bear market”. Even if people stop purchasing Safex Tokens or the price decreases due to market conditions, as long as items are selling on the marketplace then incentives are being earned independent of the Safex token or Safex Cash price.

It is worth emphasising this point once more using an example. Consider the case where $100 million worth of trade occurs on the marketplace in a single day. The 5% marketplace fee means that $5 million dollars worth of incentives are paid to token holders in the form of Safex Cash.

The number of Safex Cash paid to token holders changes depending on the cost of Safex cash, but the value does not. If Safex Cash is worth $1 then 5 million Safex Cash total are paid as incentives; If Safex Cash is worth $10 then only 500,000 are paid to token holders. In both cases, a total of $5 million dollars’ worth of Safex Cash is distributed to locked in tokens.

There is however one further complicating factor… the percentage of locked in tokens. As I have previously mentioned, a decrease in locked in Safex tokens leads to an increase in effective incentive payment for all of the locked tokens.

In a “bull market”, where the price of Safex Tokens is rapidly rising we are more likely to see investors unlock tokens to sell and take advantage of the high price of the Safex token. This situation is likely to lead to an effective increase in incentive payments for locked in tokens.

In a “bear market”, where the price of token is low or falling, I expect that people will more likely lock in their tokens to receive incentive payments and offset any capital loss they are experiencing. This situation would effectively decrease the multiplier for incentive payments per locked in token (up to a theoretical minimum of 1 if 100% of the tokens are locked in).

So, whilst the total incentive payment is independent of the price of the Safex token, the effective value of incentive per individual token could potentially be implicitly altered by current market conditions.

I will discuss this point further in the article.

The number of locked in coins

Please note that the following information is pretty close to speculation on my part. Although I have done my best to gather relevant data, the total number of users who are performing token burns, the number of lost tokens, and the number of tokens in circulation (i.e. not locked in) is an unknown.

As such, the predictions below are my “gut feeling” and you should not base any financial decisions on them. Having said that, let’s make some assumptions and see where we end up…

a) “Lost” tokens:

Over time a significant portion of cryptocurrency can become “lost”. This may occur when a hard drive containing a wallet dies and the private keys and wallet.dat are not backed up. Crypto can also be lost if they are sent to the wrong receiving address (we have heard multiple stories of people sending coins to a BTC address, rather than a Safex address) or the address may contain a typo.

There is also the risk of loss of tokens if a holder dies without leaving a trusted relative or lawyer with instructions on how to access the crypto funds. Such a situation arose recently when one of the founders of Ripple (XRP), Matthew Mellon, died suddenly.

It is estimated that between 17 – 23% of Bitcoin (BTC) has been lost over the years which, over the 10 years in which BTC has existed, amounts to an average of 1.8 – 2.4% loss per year (it is unclear what the actual value per year would be, this crude approximation is the best we can do). Note that this approximation assumes that Satoshi’s ~1 million BTC are lost. If we do not make this assumption then the percentage of lost BTC is 10 – 17%, or around 1 – 1.8% loss per year on average.

It is difficult to know whether more BTC would have been lost early in its life when users were generally more tech savvy but BTC was almost worthless, or more recently, when BTC is very valuable (and hence, people are more likely to take extra care when transferring) but many users can be… technologically challenged.

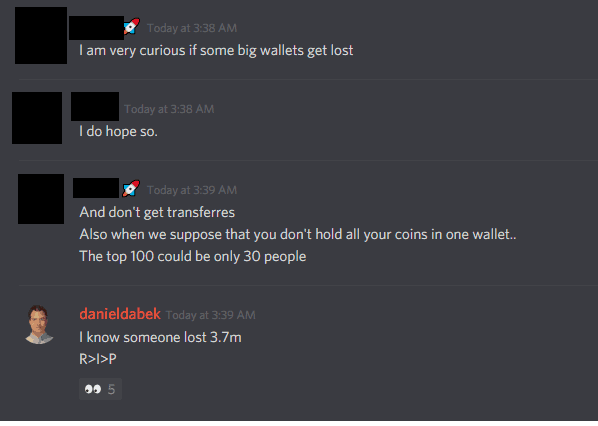

One thing we know for sure; thus far at least 3.7 million Safex tokens have already been lost according to the screenshot below from the Safex Discord:

The Safex crowdfund was approximately 2 years and 6 months ago (at the time of writing). If we assume a similar loss rate of Safex tokens as BTC then we can speculate that

Approximately 2 – 6% of Safex Tokens are currently “lost”

b) Tokens that don’t make it to the new blockchain:

Now that the Safex mainnet has been released we are able to transfer our Safex tokens from the Omni blockchain to the new Safex one. The understanding is that there will be a limited time (approximately one year) in which tokens must be migrated to the new blockchain. Any tokens that remain on the Omni blockchain after this time will be unredeemable (i.e. they will effectively be lost).

There are (at least) three main reasons why tokens will not make it over to the new blockchain;

- They are lost (see previous section). Obviously any tokens that are currently lost can not be migrated to the new blockchain.

- Token holders either do not know about the blockchain migration, or they have forgotten. At last count, just over 1500 Safex addresses on the Omni blockchain contained 1000 or less tokens. It is not a huge leap to assume that many of these wallets have been forgotten, although the total number of Safex within is a relatively small percentage of total Safex supply.

- The Bittrex/Cryptopia tokens. This is a complete wildcard. At the time that Safex was delisted from Bittrex and Cryptopia there was a limited time which users were given to withdraw their Safex tokens. This time has now passed, but the Bittrex wallet is still the largest Safex wallet, and accounts for 5.8% of Safex supply (see wallet list).

It is unclear if these tokens will make it across to the new blockchain or not. If they are not migrated to the new blockchain then this is a huge net benefit to those investors who do migrate and lock in their tokens to receive incentives.

Not only will investors receive a larger net incentive payment, but the effective lower total supply of Safex tokens should in theory raise the value of each token itself, since supply is further reduced.

It is impossible to predict what will happen with token migration, especially with the Bittrex wallet situation. In one year we will know for sure how much the supply has been culled by the blockchain migration, and we can more accurately assess how this has affected the total percentage of “locked in” tokens that are receiving incentives.

c) Tokens on exchanges/in trades:

The biggest potential for unlocked tokens are ones that are actively being traded on exchanges. At present, across the 5 pairs listed on TradeSatoshi, just over 14 million Safex (around 0.65% of the total supply) are listed on the sell side of the ledger.

We might expect that this would increase once we are listed on a large exchange, once the price of Safex token increases, and once incentive payments begin (since this is expected to greatly increase demand for the Safex token).

To approximate this source of unlocked tokens I studied “Proof-Of-Stake” (POS) coins, since these coins also give “incentive payments” for holding coins in a wallet. Many of these coins also include Masternodes as a secondary way of earning incentive payments.

I accessed data on the number of coins in Masternodes, the number of coins staking, and other “locked” coins, such as in a bounty/dev fund, or in burn addresses. I accessed this data multiple times (31st July, 7th, 12th, 17th August) to better understand the variance in locked coin amount.

We assume that “lost” coins are not currently being staked or locked in Masternodes, hence they are included in the number of coins “in circulation”.

My main data sources were:

- https://masternodes.online

- https://masternodes.pro

- https://dcrstats.com/

- https://178.254.23.111/~pub/DN/DN_masternode_payments_stats.html

- https://chainz.cryptoid.info

as well as directly contacting some dev teams on Telegram and Discord.

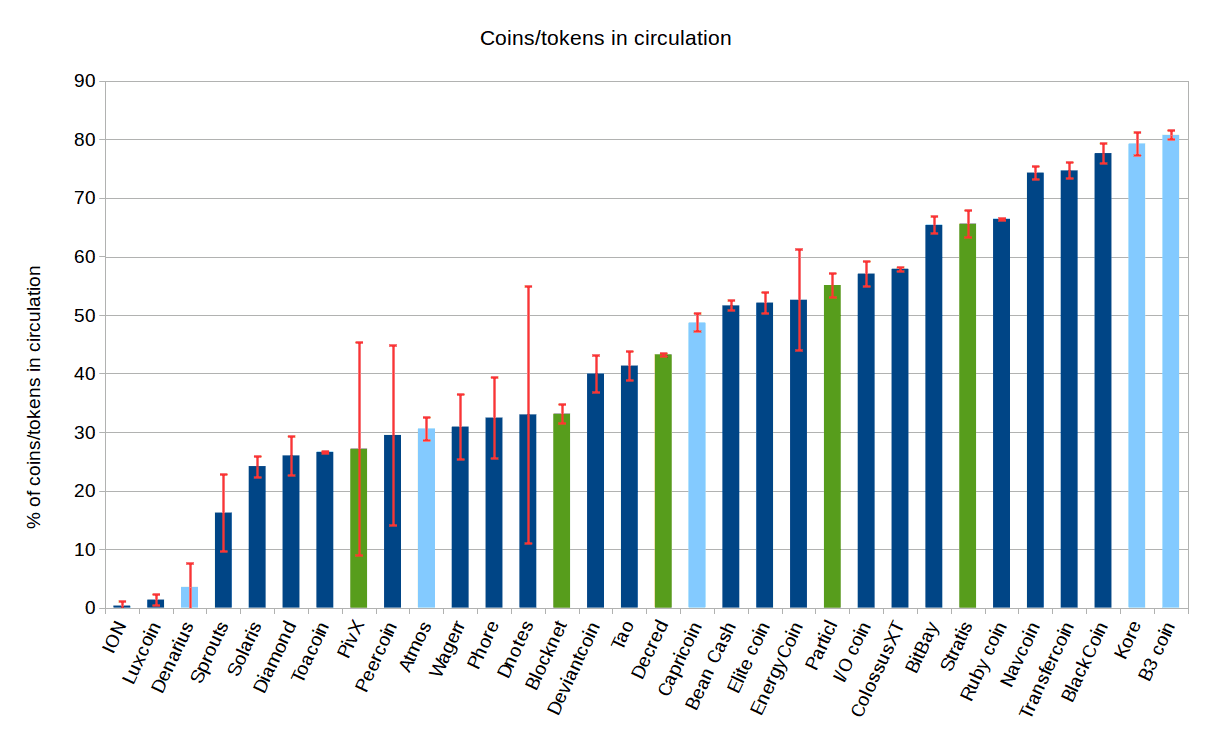

The average number of coins “in circulation” (i.e. in the “unlocked” state) and an error estimate is shown in the graph below.

Dark green bars indicate the five coins with the largest market cap (as of 31st July 2018), while light blue bars are those with the smallest market cap. From the graph above we note that:

- The variation in the number of “unlocked” coins in circulation is massive. While four of the studied coins have less than 20% of coins in circulation, five have more than 70% “unlocked”.

- Some coins have very large variance in the data (e.g. PivX, Peercoin, Dnotes, EnergyCoin). This is likely from erroneous data provided by the sources listed above.

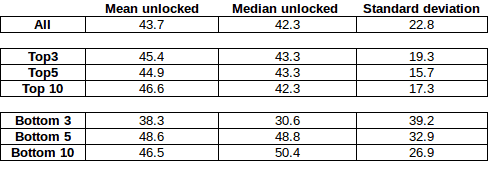

- The “average” number of “unlocked” coins in circulation is quite large. Data for this is below:

In the table above, the average percentage of “unlocked” coins is around 43%. Also shown in the table is the mean, median, and standard deviation of all of the tokens, as well as the top and bottom 3, 5, and 10 coins by market cap. The variance in the amount of tokens “unlocked” decreases as the market cap increases (i.e. more valuable coins are more consistent in the number unlocked).

At first glance, these numbers looks extremely encouraging for Safex investors. If ~40% of all coins were not locked in then the incentive payments for the locked coins would be significantly increased. However, there are a couple of caveats that we should consider.

Firstly, as mentioned, these numbers already include lost coins. If an average of 10% of coins were lost for each currency then the average of those truly in circulation would need to be adjusted by that much (although they would still not count towards incentive payments).

Secondly, it is likely that more people will “lock in” their Safex tokens for incentive earnings for a few reasons.

- Incentive payments has been a major selling point of Safex from the start and many of us will have invested mainly based on this premise.

- The lock-in mechanism for Safex is likely to be significantly simpler than for POS currencies. With POS, the wallet usually has to be left open and running all of the time. It is expected that, with Safex incentives, once tokens are locked in there will be no need to keep your wallet open and your computer running 24/7. This is likely to increase the number of locked in Safex tokens.

Considering all of the above discussion on lost tokens, tokens that do not make it across to the new blockchain, and those tokens that are being traded (and hence not locked in), the 20% lost approximation used on the Safex News incentive tool seems very reasonable.

In summary, I would personally expect the total percentage of unlocked tokens to be in the range

Total unlocked estimate: 15 – 35%

(an incentive multiplier of ~1.2 – 1.5) with some variation due to market dynamics.

Locked token – “ROI” dynamics:

Returning to the point about the interplay between market conditions and the number of locked in tokens. As I noted, while the total incentive payment is independent of the price of the Safex token, the value of incentive per individual token could potentially be implicitly altered by current market conditions.

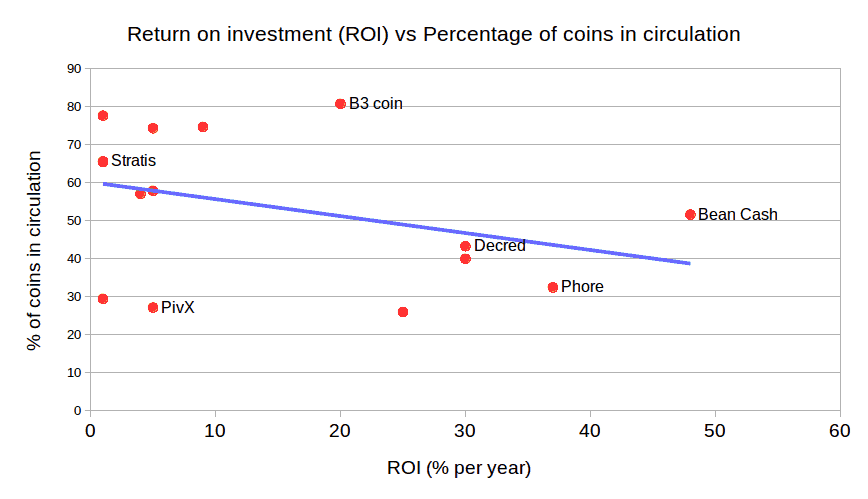

To try to find evidence of this I studied data available at https://www.poslist.org/ to compare the approximate Return On Investment (ROI) as a function of the percentage of “unlocked” coins in circulation. The graph below shows this dynamic.

In general, the trend is that the greater the ROI, the less tokens are in circulation. Stated another way, if incentives (in this case, from POS) are large enough, then more people will lock in their token to earn incentives. However, if ROI from incentives (staking) is lower, people will try to trade to earn a profit, either through pure capital gain or through “day trading” means.

This interesting dynamic adds a layer of complication to incentive payments that is difficult to predict in advance. If the price of the Safex token rises high, reducing the effective ROI (since it is more expensive to buy) then it is possible that fewer people will lock in tokens, and will trade on capital gains only. This would increase the effective incentive payout per locked token.

If, however, the Safex token is “undervalued” and the ROI is relatively large (imagine earning $1 per year from incentives when the Safex token also costs $1, an effective 100% ROI) then it is likely that a high percentage of tokens will be locked in to earn incentives.

It is worth noting that this analysis was performed in August 2018 which was during a relatively “bear” market. It would be interesting to repeat the study during the next “bull” market.

If you enjoyed this article, please consider following me https://twitter.com/znffal and Safex News https://twitter.com/SafexNews on Twitter.

Many thanks to “Astralite” for proofing this article.

Thanks you for your contribution once again. Very good research.

“we have heard multiple stories of people sending coins to a BTC address, rather than a Safex address”

Why is this an issue? SAFEX is on the BTC blockchain. Just plug the address’s private key in the safex wallet and you’ll see your coins.

This is referring to the times when people send their Safex to a Bitcoin address on an exchange. It’s a little more complicated to recover in this instance. We’ve heard of people losing a few million by doing this.